To secure growth, countries must focus on what works: clear trade rules, fiscal discipline, robust policy frameworks, and investments in productivity. The alternative is slower, more volatile economic activity. www.imf.org/en/Publicati...

14.10.2025 16:28

👍 1

🔁 0

💬 1

📌 0

Other forces are at play: AI investment is booming, echoing the dot-com era, while China's property sector struggles and fiscal pressures mount. These dynamics create a complex, uneven recovery.

14.10.2025 16:28

👍 0

🔁 0

💬 1

📌 0

Six months on, the tariff shock's impact has been smaller than expected thanks to agile supply chains and easy financial conditions. But with US tariffs still at almost 20% and tensions unresolved, the full effects will take time to unfold.

14.10.2025 16:28

👍 0

🔁 0

💬 1

📌 0

Our October WEO report is out. Global growth is expected to slow to 3.2% this year and 3.1% next year, defying fears of a sharper slowdown after the US tariff surge. Yet, this resilience masks deeper fragilities in trade, AI, and fiscal policy. imf.org/en/Blogs/Art...

14.10.2025 16:28

👍 6

🔁 0

💬 1

📌 0

New WEO chapter is out. Industrial policy can raise production in a strategic sector, but this needs to be balanced against higher consumer prices, fiscal costs, and risks of misallocation. Managing these trade-offs is key. www.imf.org/en/Publicati...

03.10.2025 14:43

👍 4

🔁 1

💬 0

📌 1

Despite these shifts, the international monetary system remains solidly anchored by the US dollar, which continues to provide global stability, even if the excess return on US foreign assets (the US 'exorbitant privilege') has declined over time. imf.org/en/Blogs/Art...

22.07.2025 17:37

👍 4

🔁 3

💬 0

📌 0

Global current account balances widened in 2024, reversing a narrowing trend. Our latest External Sector Report finds that 2/3 of this widening is excessive—driven by macroeconomic imbalances in China, the US, and the euro area. Read the full report a imf.org/en/Publicati...

22.07.2025 17:37

👍 8

🔁 3

💬 1

📌 0

Our policy recommendations call for prudence and improved collaboration. The first priority should be to restore a clear stable and predictable trade environment. Monetary policy must remain agile; rebuilding fiscal buffers is crucial, and structural reforms remain needed.

22.04.2025 15:58

👍 4

🔁 2

💬 0

📌 0

In the US, tariffs constitute a negative supply shock, with growth revised down and inflation revised up. For trading partners like China, tariffs are mostly a negative demand shock, with growth and inflation both revised down. www.imf.org/en/Publicati...

22.04.2025 15:58

👍 2

🔁 2

💬 1

📌 0

Our report presents a range of global growth outlooks: Compared to the reference forecast, growth would have been higher under the pre-April 2 alternative, while the pause on April 9, even if permanent, does not significantly alter the negative impact on global growth.

22.04.2025 15:58

👍 0

🔁 0

💬 1

📌 0

Our new WEO out. The global economy is entering a new era. Effective tariff rates reach levels not seen in a century. We project global growth at 2.8% for 2025—a major downgrade reflecting escalating trade tensions and high policy uncertainty. www.imf.org/en/Blogs/Art...

22.04.2025 15:58

👍 15

🔁 6

💬 1

📌 2

New at JIE: "Changing global linkages: A new Cold War?" by Gita Gopinath, Pierre-Olivier Gourinchas (@pgourinchas.bsky.social), Andrea F. Presbitero, Petia Topalova

https://doi.org/10.1016/j.jinteco.2024.104042

27.01.2025 16:19

👍 8

🔁 3

💬 1

📌 0

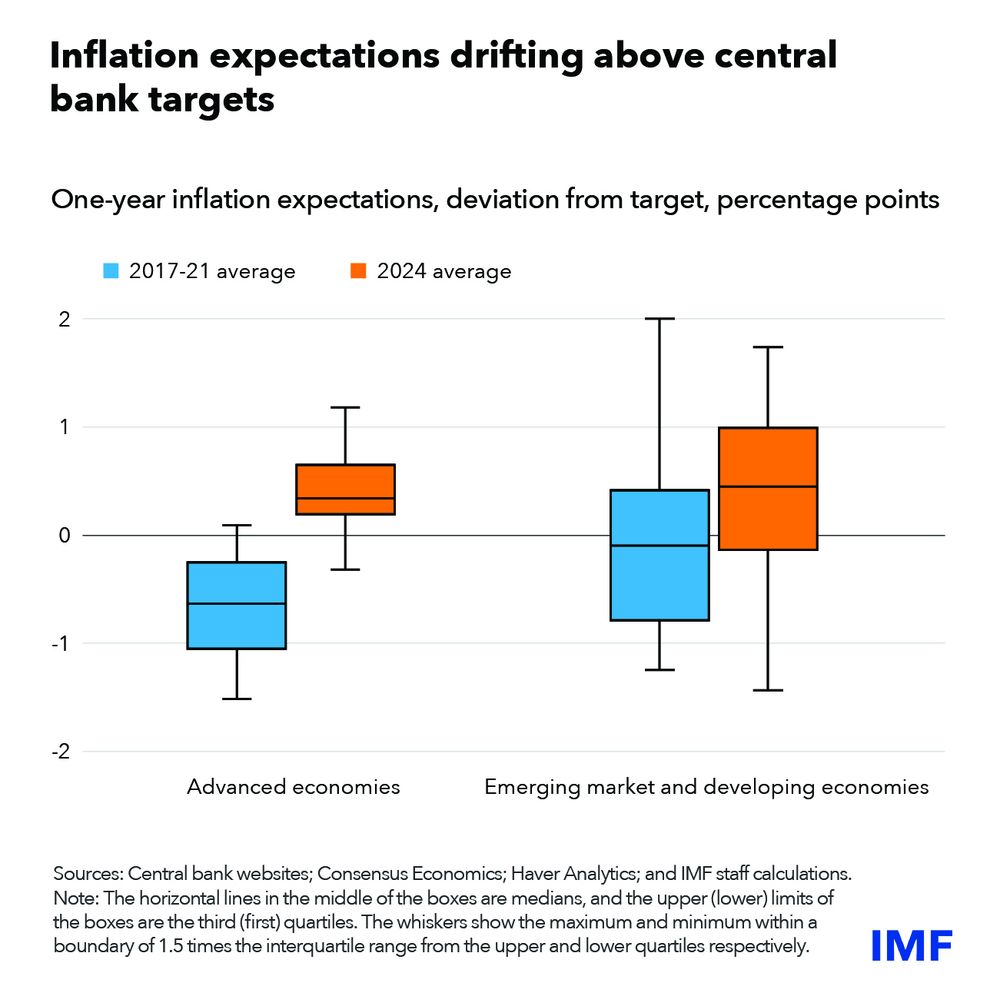

Policymakers should prioritize urgent fiscal policy adjustments and targeted structural reforms while maintaining price stability in an environment of fragile inflation expectations. Success in achieving sustainable global growth will require international cooperation. www.imf.org/en/Publicati...

17.01.2025 18:41

👍 2

🔁 1

💬 0

📌 0

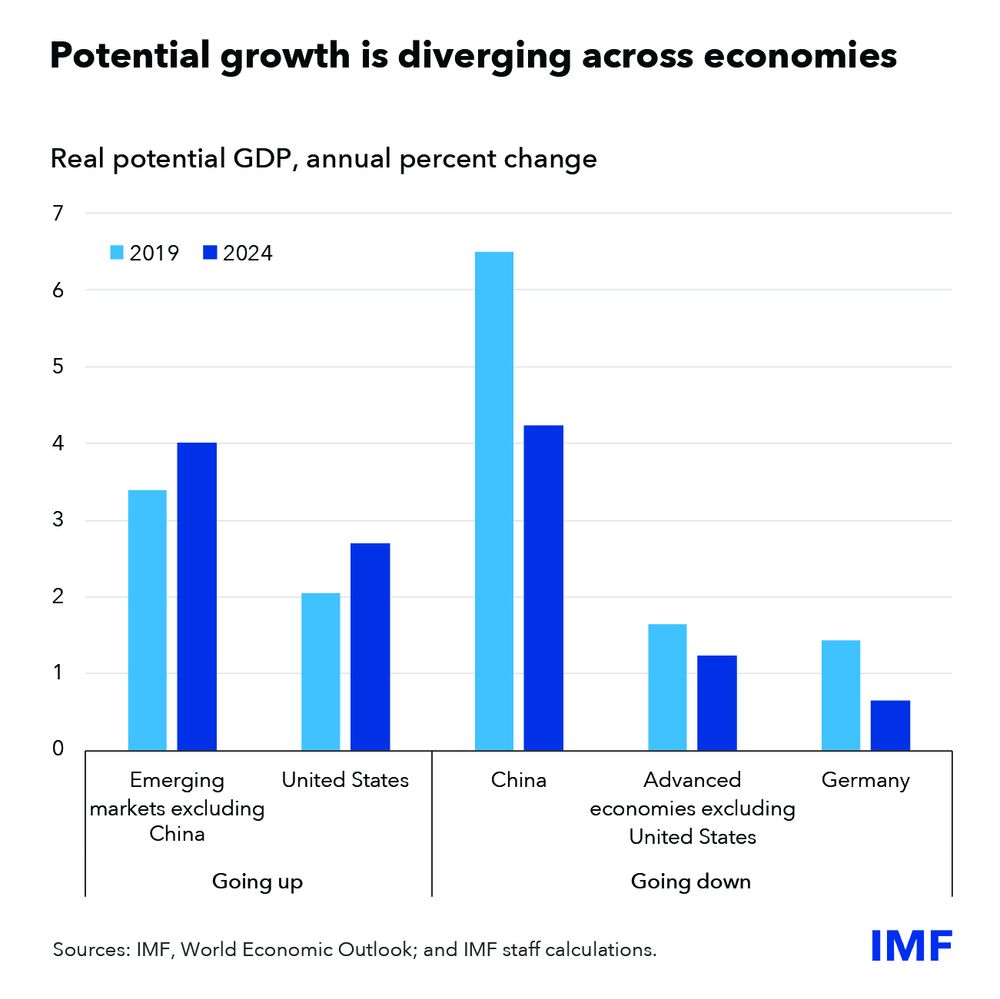

Persistent divergence between economies, reflects in part structural factors. The US shows stronger productivity growth, which has helped raise its potential growth compared to other countries. www.imf.org/en/Blogs/Art...

17.01.2025 18:41

👍 0

🔁 1

💬 1

📌 0

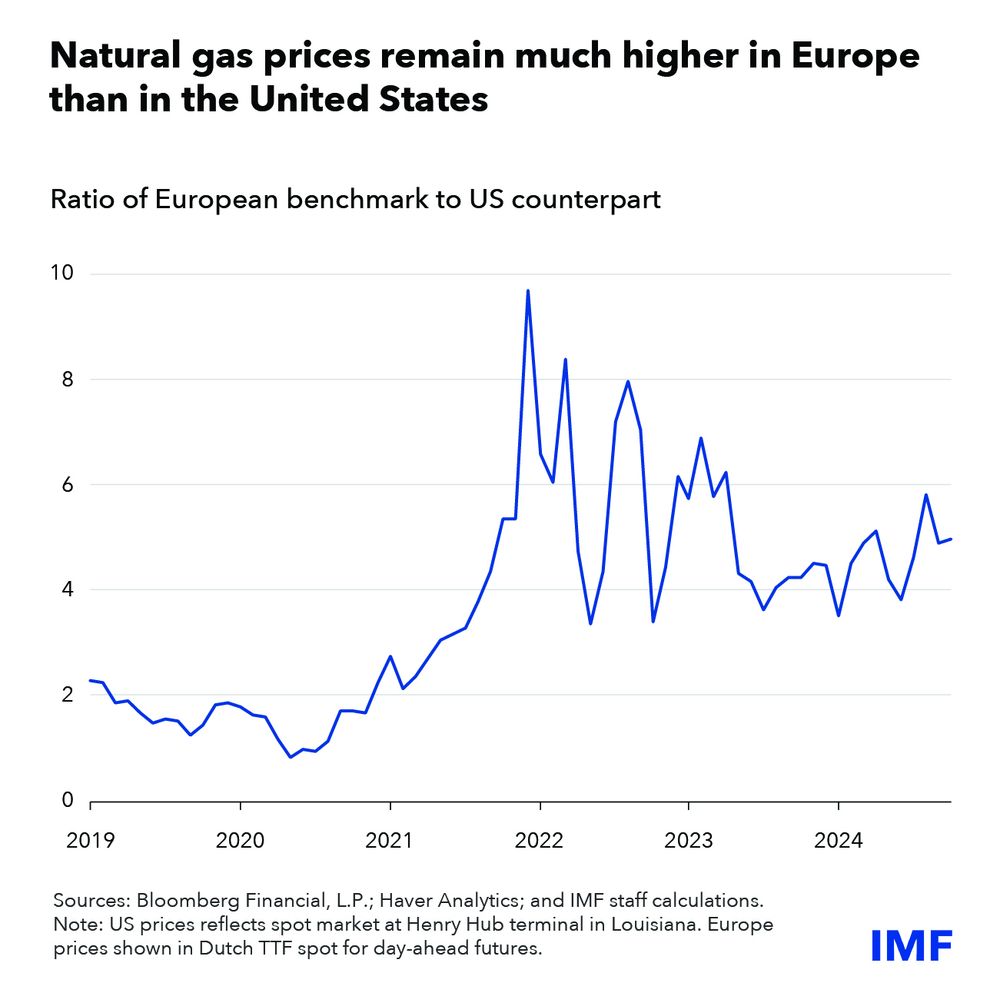

We have revised US growth up while the euro area faces headwinds from low consumer confidence and the persistence of the energy price shock. www.imf.org/en/Publicati...

17.01.2025 18:41

👍 0

🔁 0

💬 1

📌 0

Our January 2025 World Economic Outlook Update is out. Global growth will remain steady at 3.3% for 2025-26, broadly aligned with world potential growth that has substantially weakened since before the pandemic. www.imf.org/en/Blogs/Art...

17.01.2025 18:41

👍 8

🔁 4

💬 1

📌 0

Today @cepr.org & Sciences Po pay tribute to one of ours Philippe Martin, colleague and friend to many of us

And what better way than to discuss economics, trade and geopolitics

@pgourinchas.bsky.social

12.12.2024 10:01

👍 7

🔁 1

💬 0

📌 0

The likelihood of a 'soft landing', disinflation without a major slowdown in economic activity, has increased. This is particularly the case in the United States, where we now forecast a modest increase in unemployment from 3.6% to 3.9% by 2025. 3/6

14.10.2023 14:43

👍 1

🔁 0

💬 0

📌 0

Our advice to policymakers? - Remain focused on price stability - Rebuild fiscal buffers - Reforms to boost productivity and fight dimming MT growth prospects - Improve international cooperation - Prevent costly geoeconomic fragmentation bit.ly/3Q4BMFc 6/6

14.10.2023 14:42

👍 1

🔁 0

💬 0

📌 0

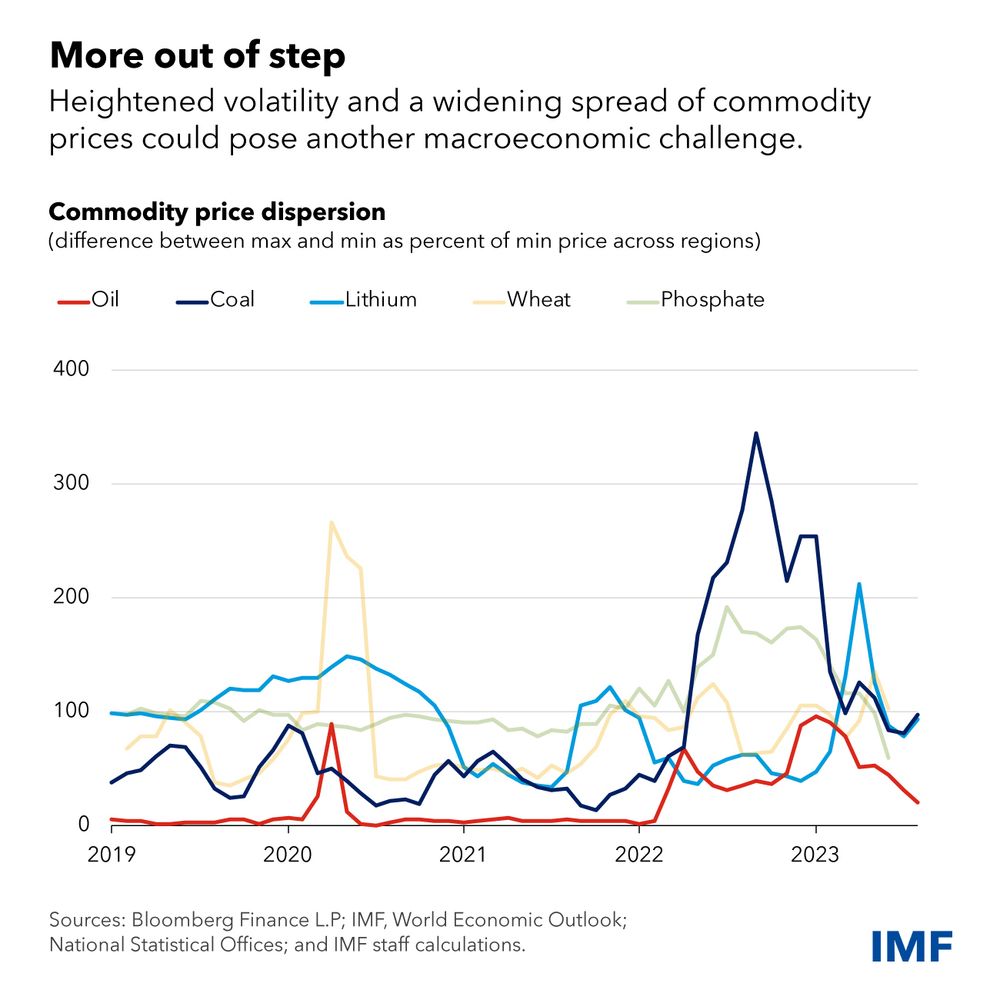

Commodity prices could become more volatile amid climate and geopolitical shocks, posing a serious risk to the disinflation path. Higher energy & food prices would bring greater hardship to low-income countries. Economic decoupling could also affect the climate transition. 5/6

14.10.2023 14:41

👍 0

🔁 0

💬 1

📌 0

Risks to the global economy persist. China's real estate crisis could intensify, posing a complex policy challenge. But it is important for China's economy to pivot away from growth driven by credit to the real estate sector. bit.ly/3PPpm2H 4/6

14.10.2023 14:39

👍 0

🔁 0

💬 1

📌 0

The likelihood of a 'soft landing', disinflation without a major slowdown in economic activity, has increased. This is particularly the case in the United States, where we now forecast a modest increase in unemployment from 3.6% to 3.9% by 2025. 3/6

14.10.2023 14:38

👍 0

🔁 0

💬 1

📌 0

Inflation is on a downward trend. Headline inflation continues to decline. Underlying 'core' inflation declines too, albeit more slowly. Most countries aren't likely to return to target inflation until 2025. bit.ly/3Q4BMFc 2/6

14.10.2023 14:35

👍 4

🔁 0

💬 2

📌 0

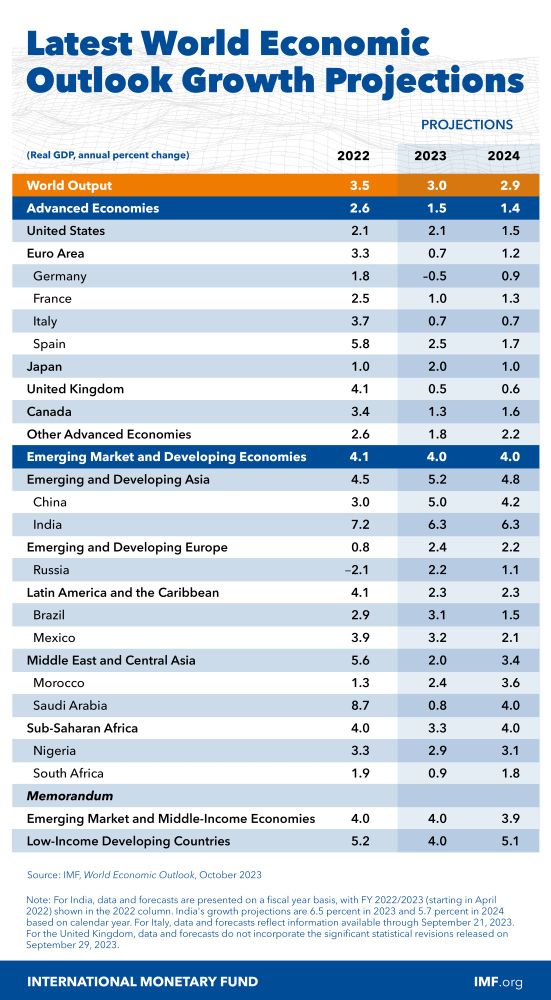

This week, we released our World Economic Outlook. With growth of 3.0% in 2023 and 2.9% in 2024, the resilience to the shocks of the past few years has been remarkable. Yet growth is slow and uneven, with growing divergences. The global economy is limping along, not sprinting. bit.ly/3PPpm2H

14.10.2023 14:33

👍 13

🔁 5

💬 3

📌 2