Fear the kink

06.03.2026 14:21

👍 2

🔁 0

💬 0

📌 0

Fear the kink

I wrote about the real INTELLIGENCE CRISIS seven years ago and it has nothing to do with AI:

www.bcaresearch.com/report-acces...

The 1974 Trade Act, on which Trump’s 10% tariff is based, does not apply in the current macro environment. A balance of payments deficit is not the same thing as a trade deficit. You cannot have a balance of payments if you have a flexible exchange rate, as the US currently does.

Something’s gotta give:

“Capex is good. It will pay for itself”

The historical record:

Poof… and it’s gone.

EVs have shown that no matter how innovative or transformational the industry, manufacturing tends to be highly competitive, low margin business. Will robots be any different?

A legitimately strong move in the ISM manufacturing index today, which is echoed in many of the PMIs abroad (so I don’t see it as a fluke). The global manufacturing sector appears to be recovering following last year’s tariff turbulence.

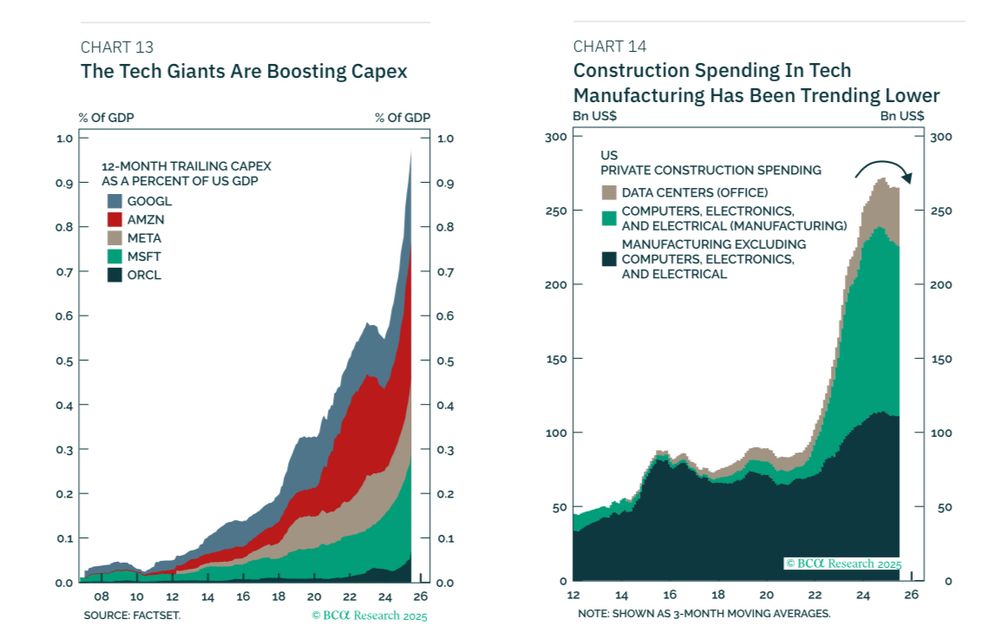

Internet traffic has grown 43% per year over the past 25 years and yet the amount of money spent on maintaining the Internet has declined as a share of GDP thanks to productivity advances. The same thing will happen to AI infrastructure spending.

I continue to be mesmerized by this chart. Internet traffic has soared over the past 25 years. Yet, the amount of investment needed to maintain the internet has declined as a share of GDP. My guess is that efficiency gains will lead to a similar outcome for AI.

Data center construction is less than 0.2% of US GDP. A lot of the hyperscaler capex consists of equipment and chips that are not produced in the US. Thus, much of what is added to “I” in the GDP accounts must get deducted via “M” (imports).

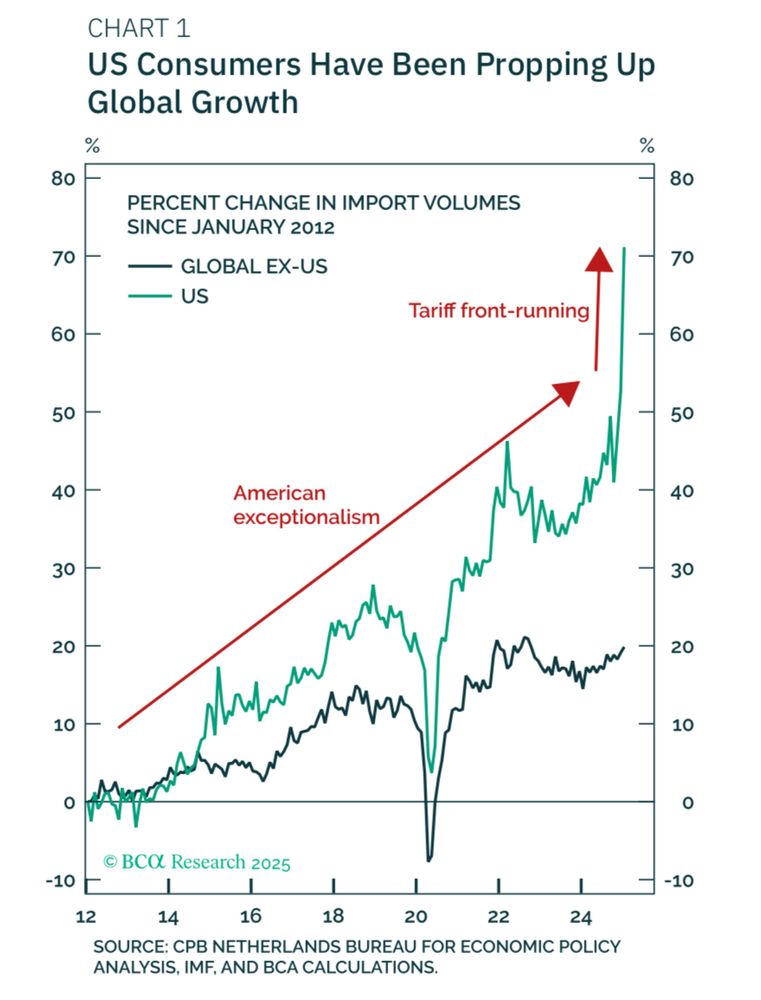

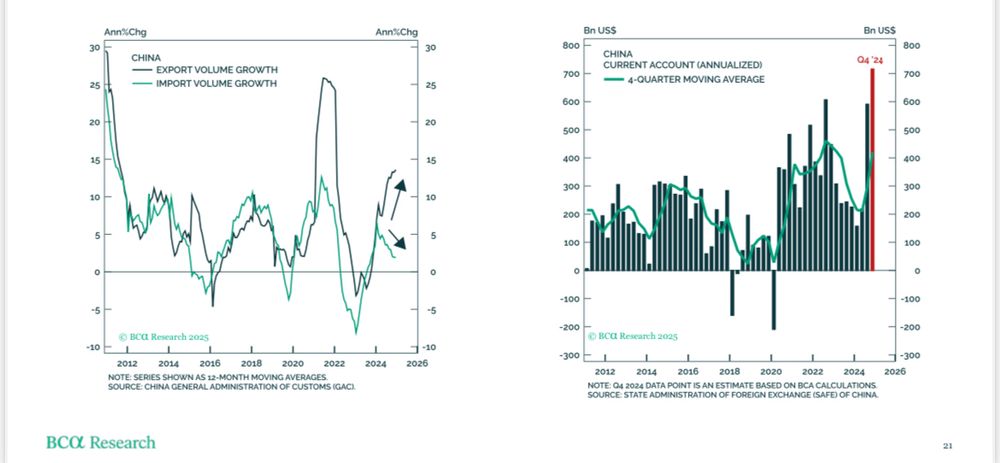

The global economy is currently benefiting from massive tariff front-running, as evidenced by the surge in imports to the US. This has temporarily propped up production in places like Europe, Canada, and China. The floor falls out next week.

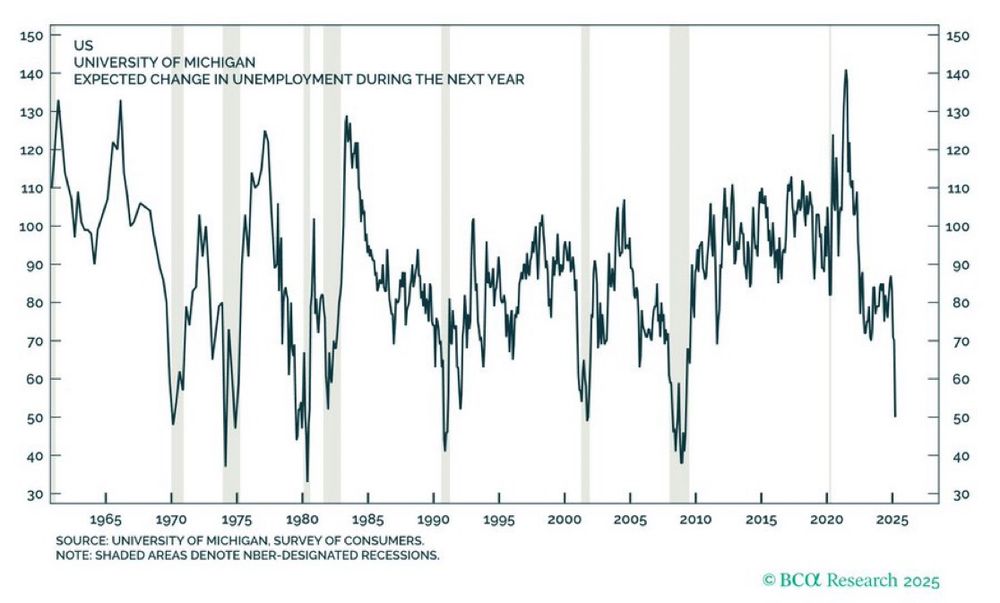

Unemployment expectations have surged to levels "never seen before" in the University of Michigan survey (outside of recessions).

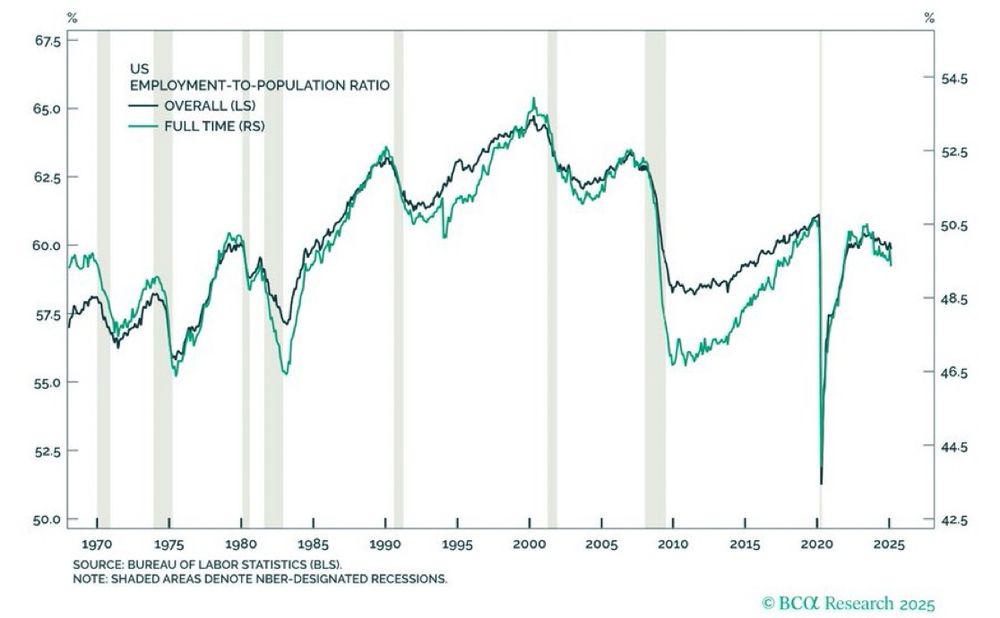

Today was a tale of two reports. The payroll report was fine, but the household report was lousy. For example, the employment/population ratio fell 0.25 ppts in February. For full-time workers, it fell 0.5 points. Usually, the E/P ratio declines in the lead-up to recessions.

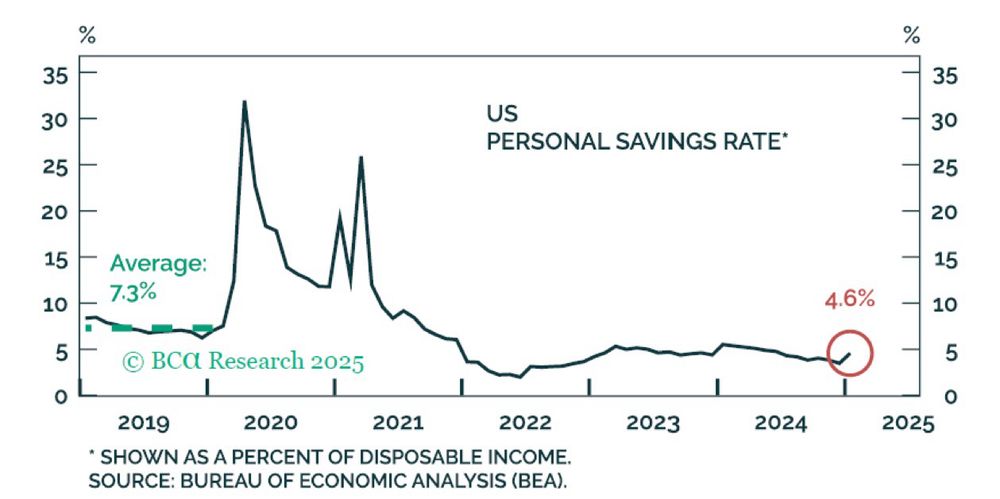

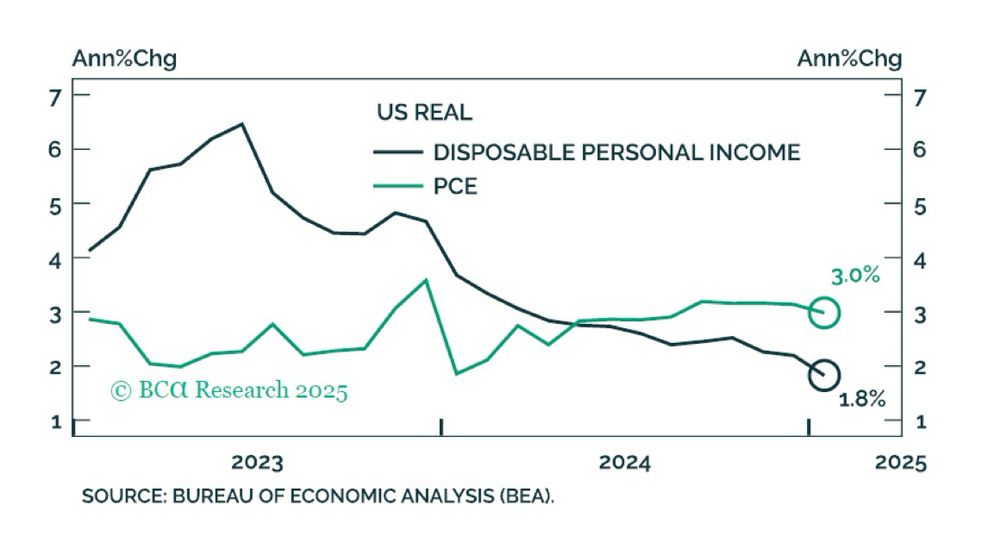

The savings rate jumped in January but remains below where it was in 2019. Even if the savings rate stabilizes at current levels, consumption growth would still fall significantly because it is currently running well above income growth.

Global manufacturing demand has benefitted from the front running of Trump’s tariffs. This can be clearly seen in the divergence between Chinese import and export growth. As this effect goes into reverse, manufacturing activity will start to weaken again.

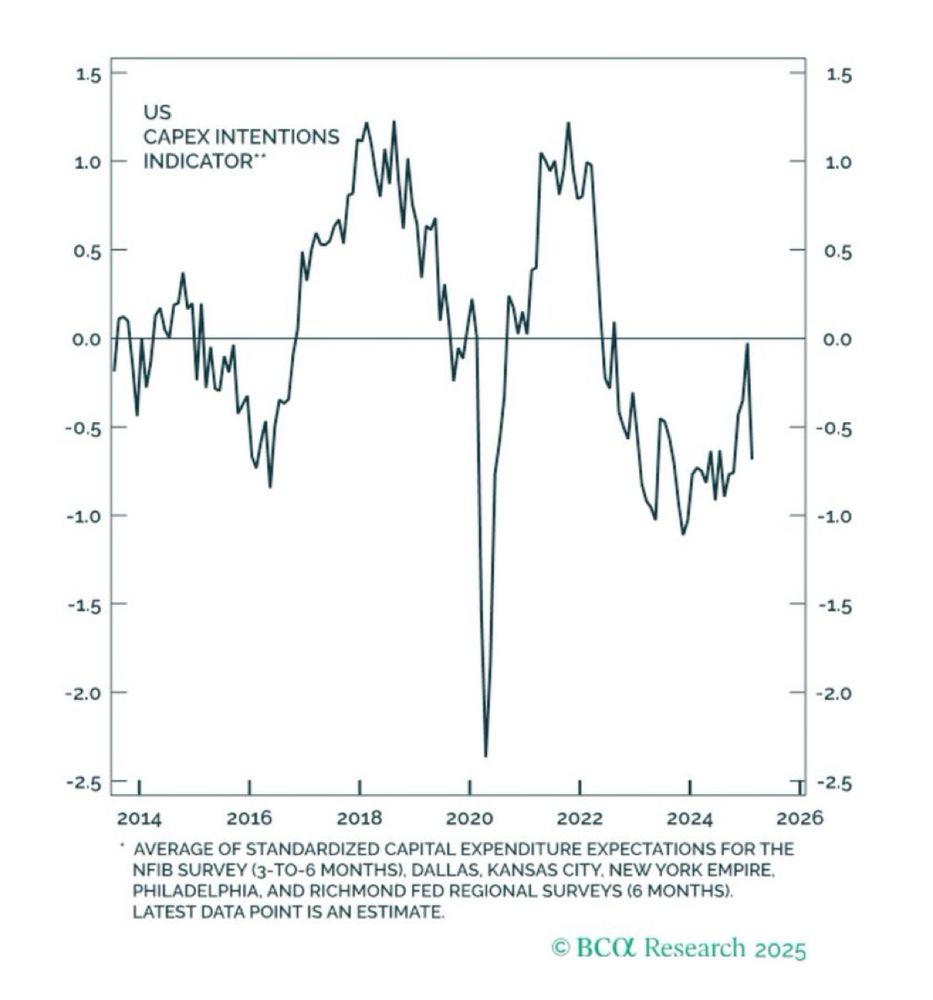

After briefly surging after Trump’s election victory, capex intentions have fallen back into contractionary territory. Sad!

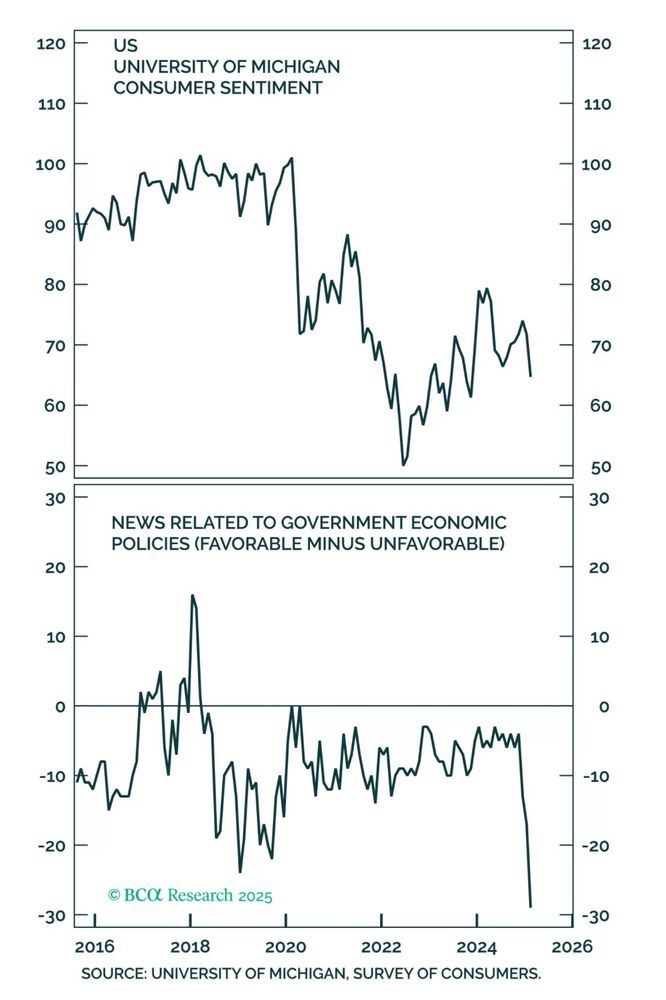

The perception that government policy has gone astray has been the main driver of the recent decline in consumer confidence in the University of Michigan survey.

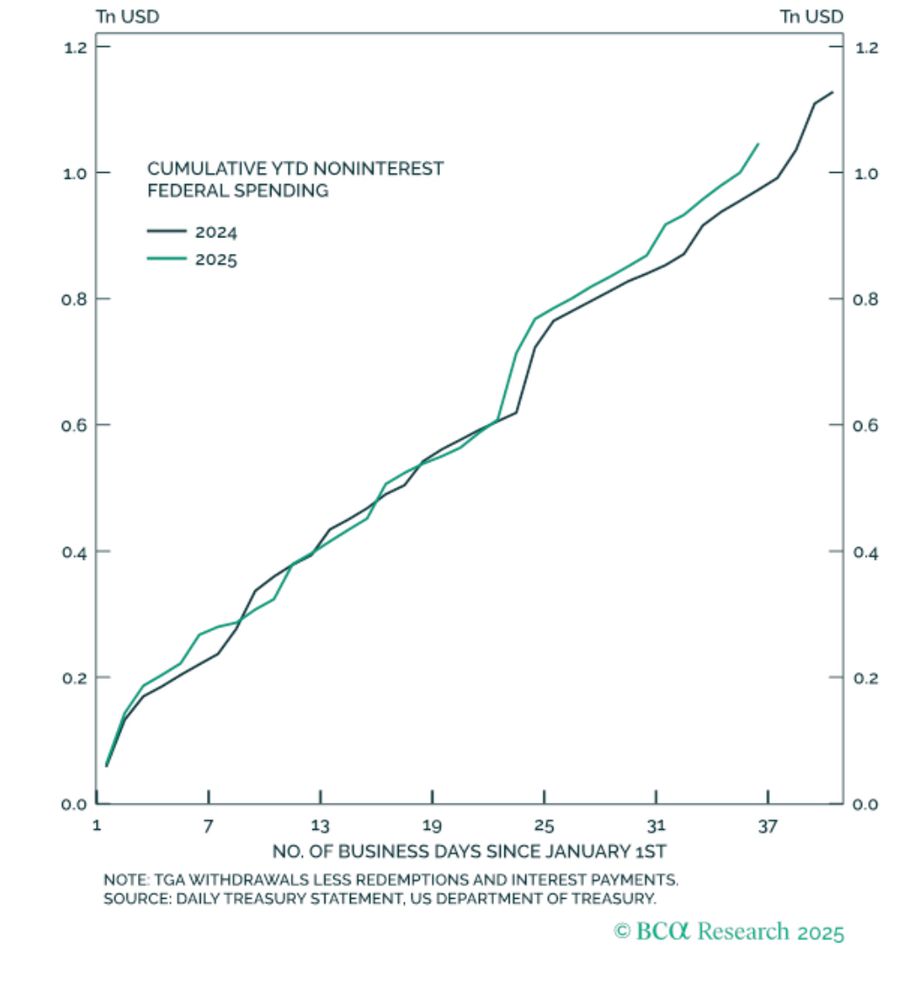

Despite all the DOGE bluster, government spending is trending higher in 2025 than in 2024.

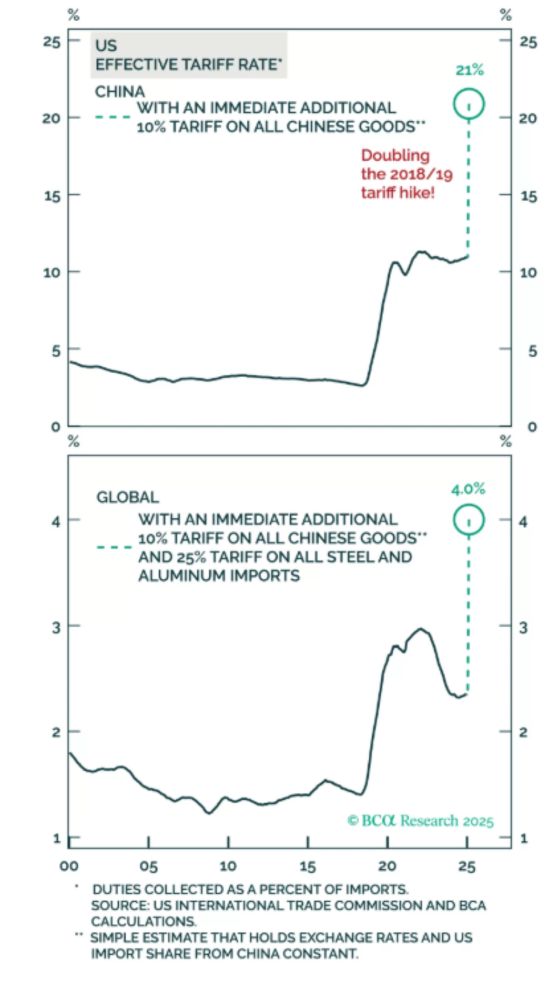

With Trump set to further increase tariffs later today, it’s worth noting that the effective US tariff rate has already risen over the past few weeks as much as it did during the entirety of Trump’s first term.